Central financial institution digital currencies (CBDCs) are a divisive subject, however whether or not you’re keen on or hate them, they’re quickly turning into a actuality.

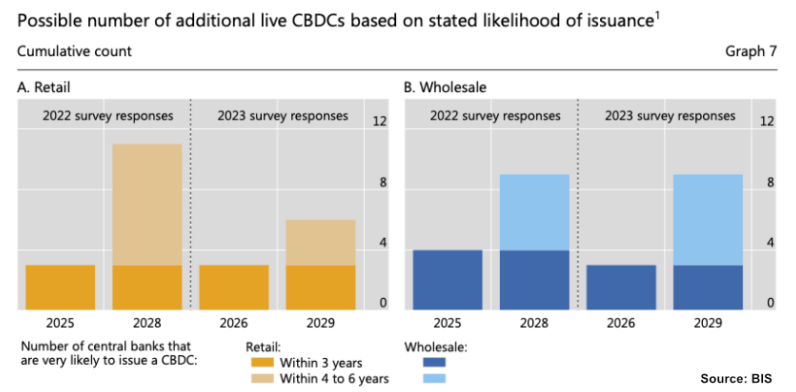

A brand new report by the Financial institution for Worldwide Settlements (BIS) reveals that the variety of central banks exploring CBDCs elevated from 93% in 2022 to 94% in 2023. The identical survey confirmed a pointy improve in CBDC pilot packages since final 12 months.

Whereas the variety of retail CBDCs issued by 2029 is ready to lower, it’s full steam forward concerning wholesale CBDCs. For the latter, the highest priorities are interoperability with home funds, programmable funds, programmable cash and interoperability with different CBDCs, in keeping with the BIS report.

mBridge cross-border CBDC platform is progressing

Whereas most central banks are actually exploring CBDCs and testing how they may work, the BIS Innovation Hub has moved the mBridge cross-border funds platform into the Minimal Viable Product (MVP) stage.

A check transaction between China and the United Arab Emirates was accomplished in January, and the central banks of China, Hong Kong, Thailand, the UAE and Saudi Arabia are already on board.

mBridge makes use of a private-permissioned blockchain with every taking part central financial institution operating nodes and validating transactions. It permits for immediate settlement between central banks of their respective CBDCs, whereas at present, it might probably take a number of days and a number of intermediaries earlier than settlement happens.

Are CBDCs good or unhealthy?

Like most know-how, they’re a double-edged sword. They’re additionally multi-faceted, having monetary, political and technological implications.

On the optimistic facet, CBDCs will allow programmable cash, which means welfare funds might be programmed to allow them to solely be spent and used for his or her meant goal. They’ll additionally usher in higher monetary transparency, making it simpler for legislation enforcement to detect and clamp down on crime.

The negatives of CBDCs can’t be ignored, although. Liberty advocates fear about monetary surveillance straight out of 1984, the flexibility for governments to freeze wallets and confiscate funds of dissidents and political rivals, and the overall lack of privateness that comes with utilizing paper cash and cash.

Central banks have famous the general public’s issues about CBDCs and tried to reassure them. The German Bundesbank not too long ago clarified that CBDCs would defend residents’ privateness and wouldn’t substitute different fee strategies, resembling bank cards and money. Nevertheless, CBDC critics are nonetheless skeptical.

An alternate ‘center manner’

CBDCs aren’t an issue in and of themselves; it’s the central bank-controlled ledgers they’ll run on that spook folks. Central banks operating the nodes will give them nearly unchecked energy.

Since CBDCs appear inevitable, a proposed center manner is to concern them on scalable public blockchains like BSV. Being a proof-of-work (PoW) blockchain, no group of central banks may have full management of the community. Different nodes run by non-public pursuits may ‘veto’ any strikes seen as unlawful, and community guidelines balancing the wants of each CBDC issuers and customers could possibly be agreed on and enforced by all.

Since nodes on PoW blockchains require huge portions of electrical energy, it’s inconceivable for them to stay nameless. Everybody may confirm who’s operating the nodes, and thus, they might be each topic to authorized orders of their jurisdictions (e.g., they may freeze funds in instances of precise crime) whereas everybody may confirm who they’re, which means entities like North Korea or the Central Intelligence Company (CIA) couldn’t take over the community utilizing Sybil assaults.

Issuing CBDCs on a scalable utility blockchain like BSV is the center manner—the entire effectivity and transparency of peer-to-peer funds with instantaneous settlement might be realized, whereas on the identical time, issues about authorities management and lack of privateness might be assuaged.

Then once more, maybe that’s not what the powers need. It’s as much as the folks to petition them and persuade them that CBDCs are solely acceptable if the ledgers they run on are distributed and out of the management of any single or tightly-knit group of entities. It’s all about belief, and BSV was designed to allow that.

Different benefits of CBDCS on a public ledger

Larger privateness and no central management are two of the advantages of public blockchains. But, there are different benefits that each CBDC critics and parts may benefit from.

Chief amongst these is interoperability between CBDCs and apps. In a permissionless system, CBDCs could possibly be utilized in all of the functions constructed on the ledger they run on, supplied the app creators design them to be appropriate. Suppose CBDCs on a closed intranet community versus on the highest web.

All of a sudden, CBDCs change into helpful for rather more than simply P2P funds between central banks and money transactions between folks in the true world. On a public, scalable blockchain, they could possibly be utilized in video games, social media platforms, communication apps, decentralized finance (DeFi) and different blockchain-based functions. From micropayments value fractions of a cent to giant settlements, CBDCs would all of the sudden have innumerable use instances.

For this to be potential, they need to run on a scalable, permissionless, PoW ledger that anybody can construct on. The primary main CBDC to make that call will doubtless achieve adoption shortly and thus win the race to be the CBDC of the longer term.

To study extra about central financial institution digital currencies and a number of the design choices that have to be thought-about when creating and launching it, learn nChain’s CBDC playbook.

Watch: CBDCs are extra than simply digital cash