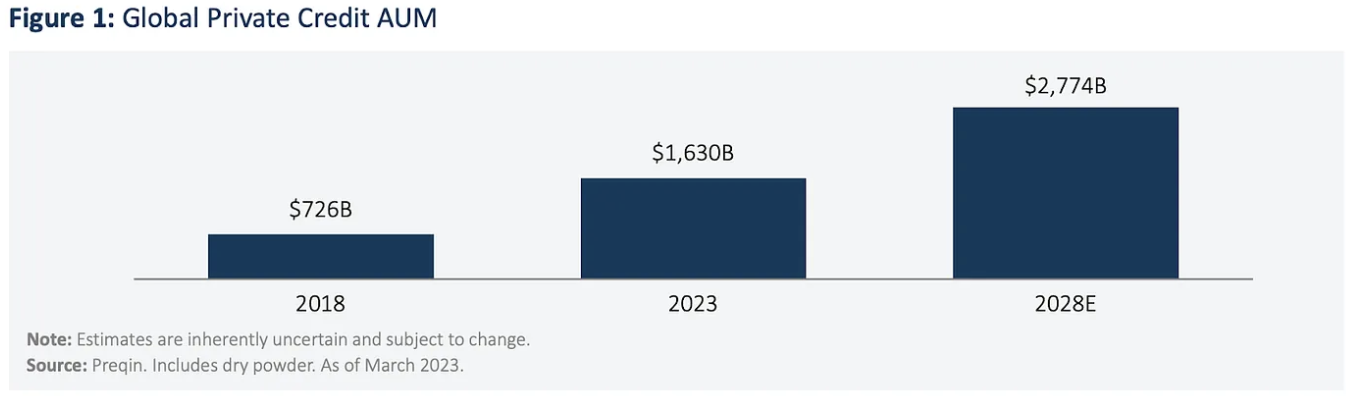

Because the World Monetary Disaster (GFC) in 2008, the expansion of the personal credit score area has been a key theme inside the various funding administration business. In keeping with TPG Angelo Gordon, personal credit score methods grew from $726 billion in international AUM in 2018 to ~$1.6 trillion in 2023. Surveys of market observers and contributors recommend {that a} majority of allocators globally intend to extend or considerably enhance their allocations to this area, leading to an anticipated $2.8 trillion in personal credit score property underneath administration by 2028:

World Non-public Credit score AUM

Supply: TPG

To what can this demonstrable development be attributed?

Because of the GFC, banks confronted elevated regulatory necessities and capital constraints, dramatically lowering their lending capacities. This has been particularly the case for asset-backed finance (ABF) or specialty credit score, which traditionally has been much less standardized and comparatively extra advanced to quantify or seize by way of information historical past, scores, and many others.

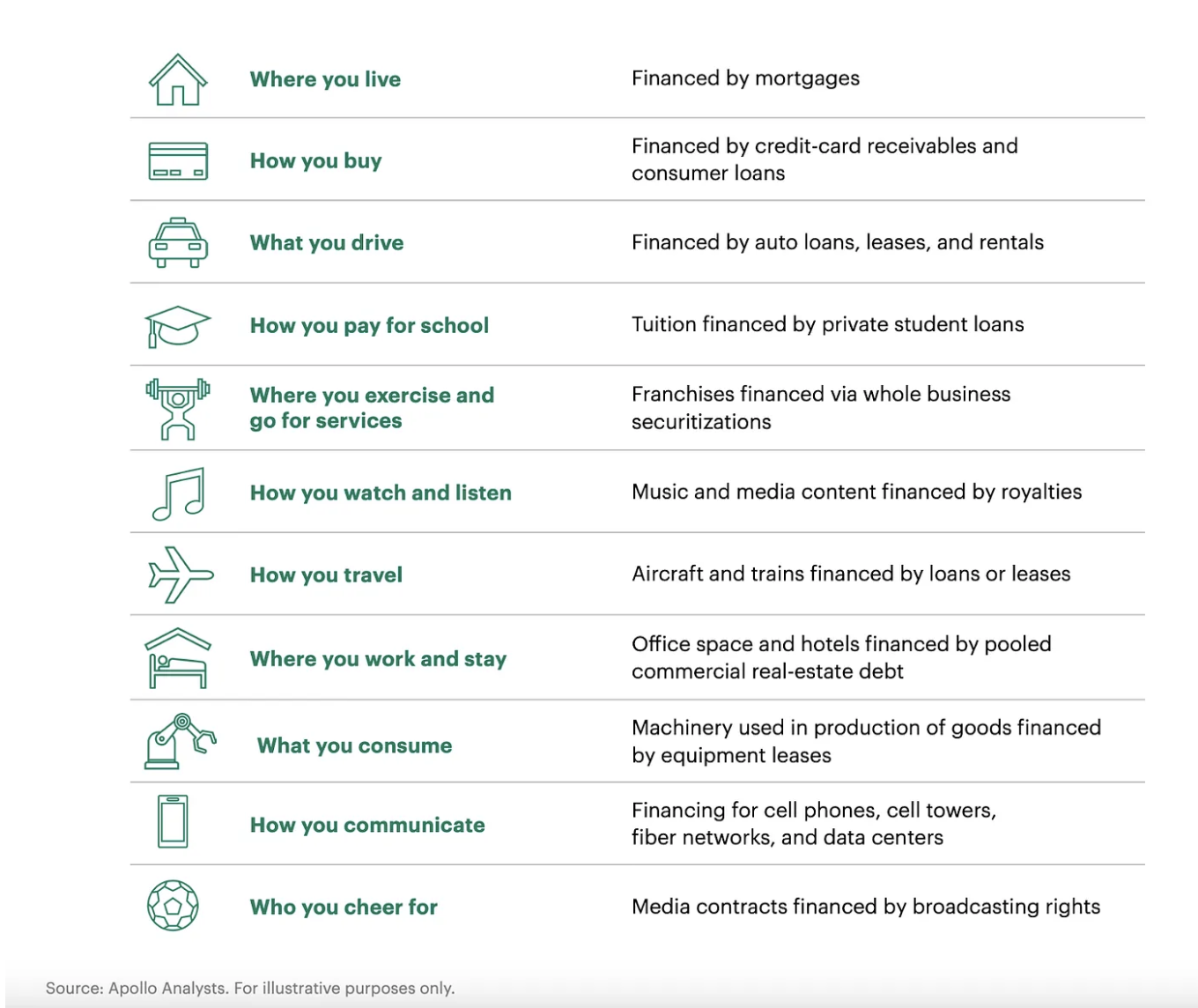

Outlining ABF

Not like company credit score, ABF depends on extra than simply the total religion and credit score of a borrowing enterprise for reimbursement. Apollo World Administration (“Apollo”) defines ABF as “lending wherein a mortgage is supported first by the contractual money flows of a pool of property owned by a limited-purpose borrower, after which by the liquidation of these property themselves.” To that finish, the ABF market is considerably bigger than the company credit score market and features a entire host of credit score sorts, together with these outlined beneath:

ABF hides in plain sight.

Whereas the contraction in financial institution lending exercise was one of many direct outcomes of the GFC, eroded belief within the conventional banking system was one other. On the identical time, technological advances in cellular know-how and cloud computing, elevated enterprise capital funding, and the utilization of synthetic intelligence (AI) and machine studying (ML) to judge various information collectively led to an increase in monetary know-how (FinTech) firms disrupting quite a lot of lending markets. From LendingClub to SoFi, Upstart to Credible, a number of profitable FinTech companies have emerged over the previous decade, which, in flip, have helped gas the expansion of ABF and different personal credit score alternatives.

Among the many numerous methods ABF will be accessed, Apollo describes possession and management of originators as one of many key methods:

Proudly owning and controlling originators of ABF property are highly effective strategies to realize publicity to ABF through direct entry to proprietary deal circulation. Contributors accessing the market on this method may also achieve rights of first refusal on originated loans or leases, in addition to rights of first refusal on securitization debt, all whereas taking part within the development of the platform originator. This entry level permits for doubtlessly increased funding unfold, given the power to go on to the underlying borrower, which reduces the involvement of intermediaries. Like personal asset-backed lending, combining structuring experience and breadth of asset data permits an originator to design a versatile, risk-mitigated credit score field. This additional permits for the potential to cross-sell and repeat present enterprise and additional drive decrease potential danger, given the power to carry out direct due diligence and preserve management of the credit score documentation.

By means of a mix of fairness and debt financing, a number of various asset managers as we speak leverage this mannequin to develop and scale ABF originators whereas gaining publicity to the area.

Finally, as non-bank lenders and specialty finance firms have grown in each quantity and measurement, they’ve been not solely addressing the funding hole left by conventional financial institution lenders post-GFC (and additional exacerbated by current financial institution failures and a ‘increased for longer’ price setting) but additionally leveraging their favorable asset-liability combine, structuring experience and technological capabilities to develop into new and novel property and markets traditionally underserved by the normal banking system.

Blockchain Innovation & Alternatives in ABF

Among the many technological improvements and developments of current years, blockchain, good contracts, and tokenization have emerged as instruments to additional seize the ABF addressable market.

“My ‘aha’ second in appreciating the revolutionary capabilities of blockchain-, smart-contract, and tokenization-enabled companies got here from an article written by BlockTower Credit score Head Kevin Miao,” stated Morgan Krupetsky, Senior Director of BD Establishments and Capital Markets at Ava Labs. “In it, Kevin states that these applied sciences will be leveraged to bypass the numerous pointless third-party service suppliers that overburden the normal $14T securitization market and, subsequently, obtain a decrease capital price for debtors. Whether or not reducing the price of capital or systemically enabling entry to credit score throughout numerous industries, this upgraded know-how stack and the assorted firms constructing upon it warrant the eye of as we speak’s ABF buyers and capital suppliers.”

One such instance is Intain–a structured finance firm whose platform has processed billions in loans by its on-chain administration platform. Combining the advantages of on-chain administration and tokenization, Intain goals to facilitate environment friendly, cost-effective, and clear end-to-end asset issuance, funding, administration, and buying and selling. The corporate strives to dramatically enhance the investor and issuer expertise by bringing all stakeholders to a shared accountability platform that promotes a single supply of fact by offering transparency, continued reconciliation, and an immutable audit path.

On the investor facet, the underlying blockchain know-how can enhance the expertise by delivering real-time transparency into each single mortgage backing an funding and the power to gather returns on a extra well timed foundation. On the issuer facet, utilizing automated good contracts reduces the price of issuance by 50–100 foundation factors on common. The platform permits an 80% discount within the days it takes to validate a mortgage pool, a 65% discount within the days it takes to underwrite a deal, and a 90% discount within the days it takes to finish post-closing administration.

Trying Forward

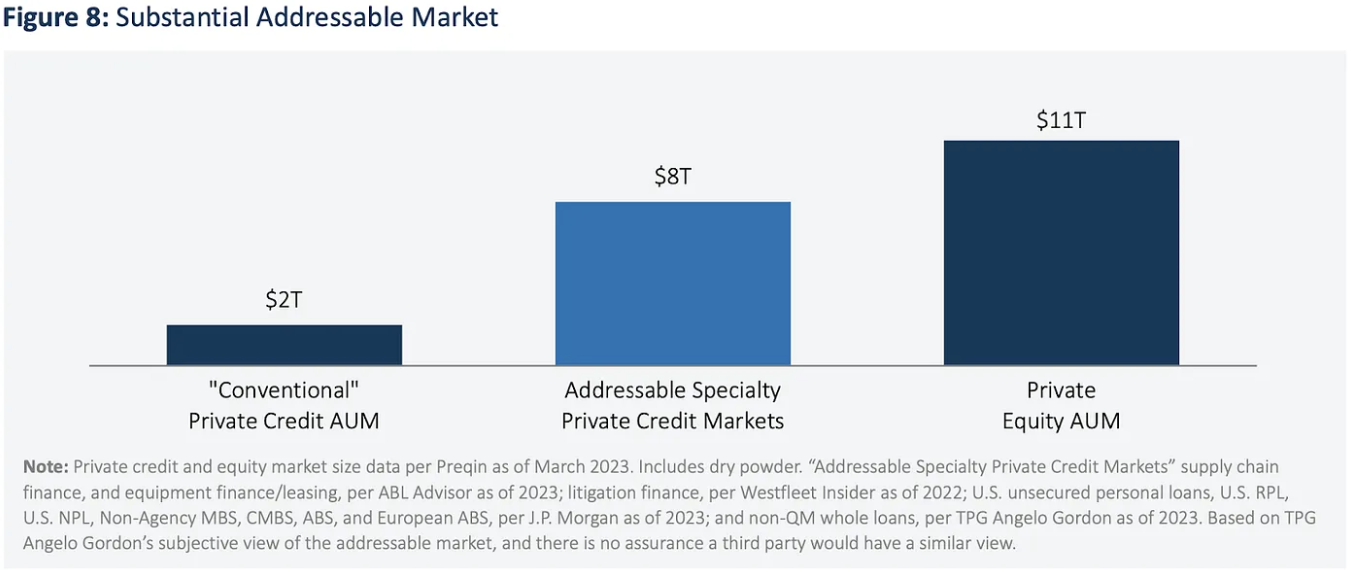

The present addressable specialty personal credit score markets stand at $8 trillion.

Substantial Addressable Market

Most of the originators constructing on blockchain as we speak–throughout house fairness, reinsurance, receivables, industrial actual property, and media/IP rights, to call just a few–convey to bear their business experience and embedded networks. They perceive acutely the business ache factors for which they’re fixing. They’re constructing blockchain-enabled companies and creating worth propositions that both don’t exist or are considerably costlier through conventional transaction, settlement, and administration rails (due to financial or operational infeasibility). As these firms supply debt financing services to scale, a lot of them stand to profit from various asset managers’ structuring experience and the power to develop alongside strategic fairness companions. This mixture of debt and fairness publicity (plus the additional benefit of potential liquid token upside) can doubtlessly present a compelling return alternative for buyers.

About Avalanche

Avalanche is a great contracts platform that scales infinitely and recurrently finalizes transactions in lower than one second. Its novel consensus protocol, Subnet infrastructure, and HyperSDK toolkit allow Web3 builders to simply launch highly effective, customized blockchain options. Construct something you need, any approach you need, on the eco-friendly blockchain designed for Web3 devs.